Don’t Let Them Debt-Fluence You!

Collective Organizing is the Way Forward + Student Debt Updates

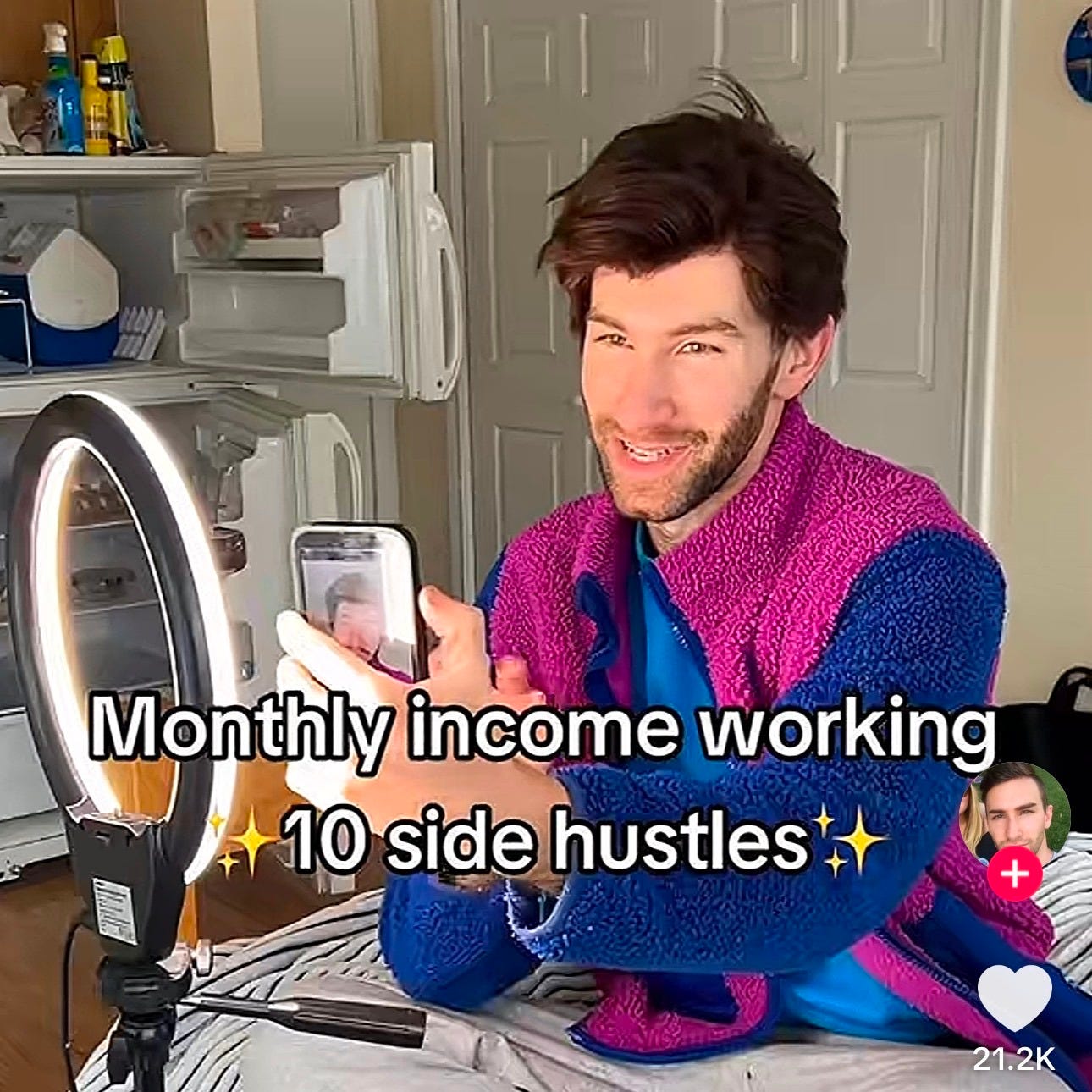

Let’s say you’ve been scrolling on TikTok or Reels. Suddenly you come across a so-called expert pushing student-debt-related advice. Funny enough, the advice almost always involves paying debt off with money you don’t have. Sometimes the advice requires you to pay a creator for more specific advice. Unfortunately, influencers who make these videos rarely grasp at the root of the student debt crisis. Instead, they’re profiting off of vulnerable debtors in desperate situations, and ushering them down a path that almost always leads to more debt.

Sociologist Dr. Amber first coined the term “debtfluencing” in a Substack post last year, arguing that an entire ecosystem of influencers has emerged online to normalize #debtpayoff culture. From advocating extreme frugality and skipping meals to juggling multiple jobs or publicly sharing massive debt balances for shock-and-awe engagement — as opposed to as a form of resistance — these debt-fluencers are rarely interested in collective solutions.

Even those who’ve built platforms with millions of supporters remain singularly focused on paying debt off as an individual pursuit, despite the deeper truth that no one should be in the red for pursuing education. No one should carry medical debt because they were diagnosed with cancer. No one should owe back rent to a behemoth corporate landlord either. What debtfluencers fail to amplify is the history of our profit-driven education, healthcare, and housing systems. They don’t disclose that lifelong student debt is virtually unheard of in most wealthy countries, or that American politicians have the legal authority to provide mass debt relief to millions. Instead, they’re obsessed with becoming one of the lucky few who beat the odds.

To make matters worse, finfluencers — debtfluencers’ partners in crime — are equally prevalent, pushing high-risk retail investing or even gambling without disclosing that they are often being paid by financial institutions. Finfluencers may also be shaping young people’s financial futures by pushing quick fixes to the affordability crisis. Spoiler: the “fix” is usually a payday loan or an expensive money management course.

Understanding unjust debt as a form of social control is essential. Americans owe $18 trillion in household debt, yet the ruling class blames it on personal failure rather than a failed system. This “personal responsibility” framework is partially pervasive because billionaires have captured our media landscape. It’s a dangerously slippery slope that leads right into the pockets of the ultra-wealthy. If debtors are framed as individuals who are simply “bad with money,” it opens the door to prejudice (an effective distraction).

For example, women and Black communities are disproportionately burdened by every type of unjust debt — “personal responsibility” logic subtly suggests that entire groups are financially irresponsible or spending recklessly. That couldn’t be further from the truth. Like poverty, unjust debt is a policy choice. If debt can accumulate for what should be public goods, then it can also be abolished.

Personal-responsibility narratives also uphold the illusion that our financial system is a level playing field and that we’ve merely lost some fairytale “fair game.” That logic justifies why a handful of billionaires hold half of the world’s wealth while shifting the blame onto individual debtors. It keeps us from building class solidarity, being outraged about wage theft — the most pervasive form of theft in the country — or recognizing that the ultra-wealthy routinely use debt to their advantage, leveraging it to generate more wealth while often avoiding taxes altogether.

Should you stay informed about what’s happening in the student debt landscape? Absolutely. But it’s equally important to remember the bigger picture: working-class Americans need full and complete debt cancellation and college, healthcare and housing for all. So if you’re an online creator courageous enough to share your debt story, why not alchemize your anger towards collective solutions?

A TikTok creator by the moniker of Cassanova Brown (@drcassanovabrown) is doing just that. He recently revealed his stressful financial situation to his 300k followers. This vulnerability inspired others online to do the same, which has resulted in what’s now called the #AgeofDisclosure series on TikTok. The series is rooted in the Black community, but open to all. Participants share job loss, high debt balances, or housing insecurity. His series has ultimately helped people develop a deeper class analysis, while remembering they’re not alone. In a world where financial stress is one of the leading drivers of suicide, and online spaces are full of smoke and mirrors, these kinds of conversations can help save lives!

If you’re ready to tell your story, to come up with collective solutions and to demand a better economic system, join us for our upcoming two part Writing Your Debt Story series. In the meantime, this post also provides insider updates in the higher education space — for debtors, by debtors. Because Debt Collective has got your back!

Student Debt Updates

Private Student Debt Collectors Pivot to Targeting Immigrant Communities

The Trump administration has re-hired the same private debt collectors previously fired by the Biden Administration for gross misconduct. Now, instead of hounding student debtors for payments they can’t afford or slapping them with exorbitant fines, these collectors have pivoted to targeting immigrants using an opaque law which was introduced by Bill Clinton, but never enforced.

According to The Lever, immigrants have been fined to the tune of 1.8 million dollars, or approximately $1000 a day, for remaining in a country that’s epically failed to enact comprehensive immigration policy. The Department of Homeland Security works in cahoots with private collectors to issue threatening letters in the hopes of scaring people to “self deport.”

What does this tell us? The Trump administration understands that unjust debt is a form of social control. This isn’t just about money, this is about using the threat of debt as leverage against vulnerable communities.

When It Comes to the SAVE Repayment Plan — Sit Tight & Stay Tuned

Although headlines have declared Biden’s SAVE plan dead, there’s much more to the story. The Trump administration’s Department of Education sent out communications claiming the SAVE plan is illegal — it’s not. Some borrowers have abandoned ship, but we’re reminding debtors to hold tight, especially because we’re currently fighting for relief promised to borrowers who spent years making payments under SAVE. For more information, watch our interview with Austin Hinkle about his work as former Section Chief of the Office of Students and Young Consumers at the CFPB as well as his work leading the ongoing litigation to protect the SAVE Plan.

Department of Education is Still Pushing a Messy Transfer to the Treasury

To refresh your memory, Linda McMahon’s plan to transfer the massive student debt portfolio to the Treasury is a terrible idea. In the past, when the Treasury tried to work with student debtors to rehabilitate 5,729 accounts, they only successfully rehabilitated 8 of those accounts. This was during a full year of trying. But that’s exactly why Trump and McMahon want to move student loans to the Treasury in the first place.

Forget Trump’s shallow interest in “affordability,” his administration wants to take money right out of working class people’s bank accounts. To make matters worse, the current undersecretary of Ed has proposed a solution to this fiasco: he wants to “modernize” the process, which means having AI do the dirty work. But AI isn’t a viable solution to their mismanagement of the student loan portfolio.

We need to call on the Trump administration to implement a one-year pause on federal student loan debt payments and collection services for all federal student debtors. Sign this petition and share far and wide!

Federal Student Aid FSA in a Hiring Blitz

FSA is looking to hire exactly 334 people to process the remaining backlog of roughly 300,000 borrower defense claims. Ironically, that number 334, is the exact number of people that FSA got rid of through the “reduction in force” in the early stages of this Trump administration. You really can’t make this shit up.

THIS Senate Vote Could Protect PSLF

The Trump administration has proposed a new rule that effectively says public service workers must align with the administration’s political views or risk losing their path to a debt-free future. That has serious consequences — not just financially, but for democracy and public service itself.

The right wing knows an indebted doctor, an organizer in fear of wage garnishment, or a teacher in danger of defaulting on her student loan is easier to control than a worker without debt. Compare this new rule to the fact that the Trump administration offered a pathway to student debt relief to recruit ICE agents and it becomes abundantly clear what the right’s vision for the future is — and it’s bleak.

Here’s the good news: Trump’s new PSLF rule can be overturned through the Congressional Review Act (CRA), but only if enough senators act now.

Debt Collective and our allies secured 32 Senate Democrats to call for a CRA vote. This is a great time for Dems to advocate for their constituents and protect one of the few pathways to relief for people who’ve devoted their lives to public service.

Help us hold Congress accountable. Contact your Senators and urge them to support a CRA vote to protect PSLF immediately.

“Just Go Into the Trades”

Don’t want to be burdened by student debt? Go into the trades, they say. Well, as we’ve previously stated, Trade schools are also debt trap. Now you have an awesome article you can send your great-aunt when she suggests you become an electrician instead of studying philosophy. Because the real question is: why can’t you do both without going into debt for the rest of your life?

Visit DebtCollective.org to join our upcoming calls or to become a member.

| A guest post by

|

The reasoning of these debtfluencers is literally backwards. Yes, they participate in the gig economy to repay debt; but a major function (and, arguably, purpose) of debt is to push people into the gig economy.