Breaking: Trump Unveils New Credit Score for ‘True Patriots’ (satire)

Bootlicking Gets a Boost With this New Way to Control People’s Financial Lives

PRESS RELEASE: The Administration that brought you Official Trump Coin, Trump Accounts (aka 401 pre-Ks), and 50-year mortgages has created a new financial tool that will continue to Make America Rich and Safe Again.

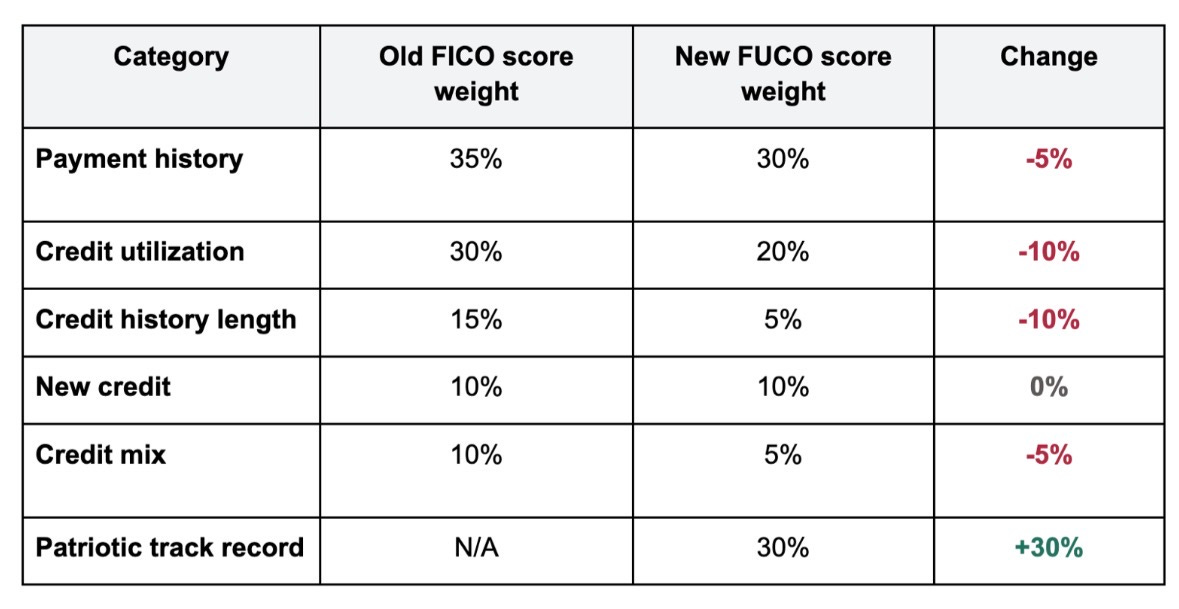

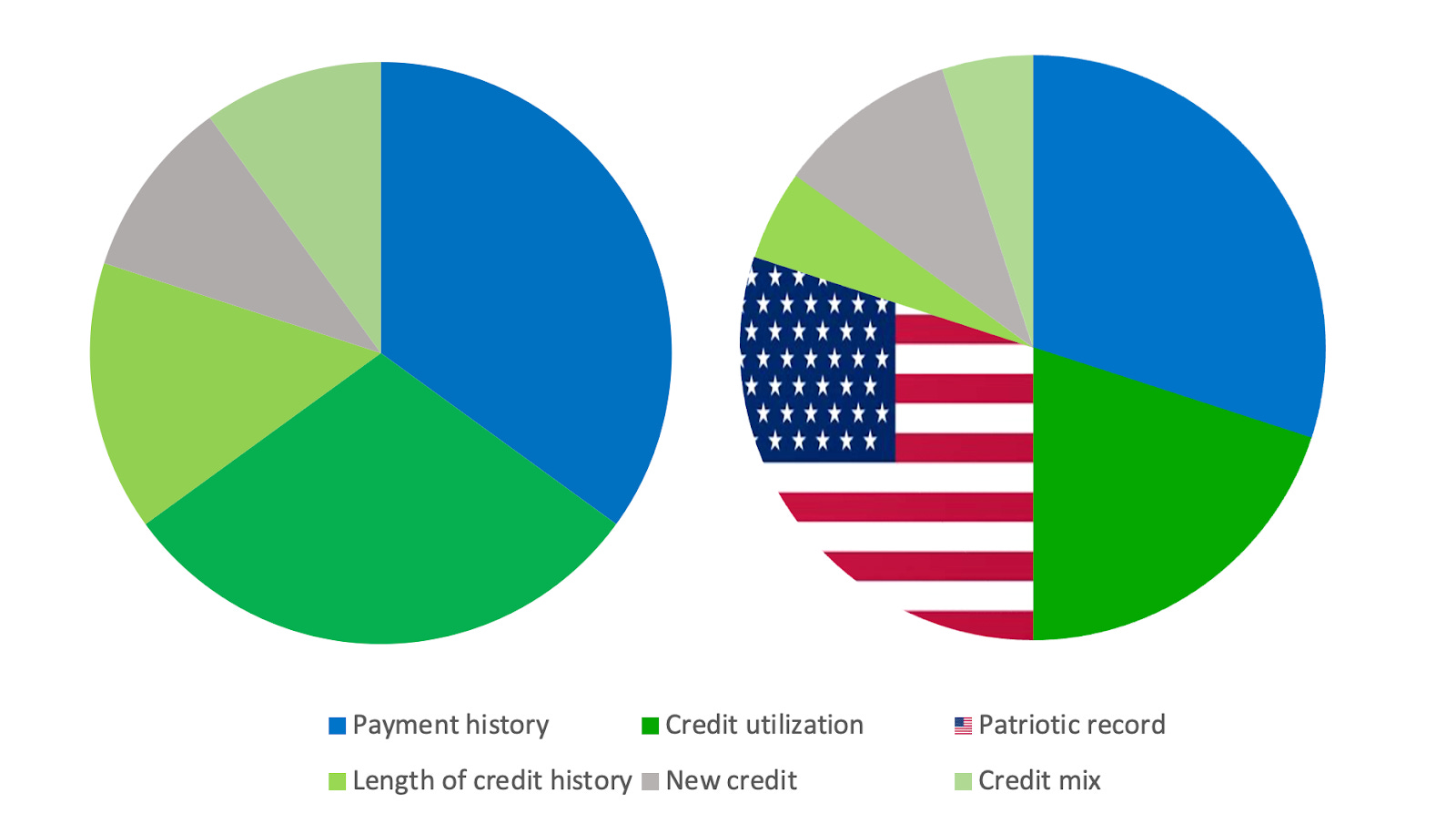

Thanks to a Historic Private-Public Partnership, your FICO score will now become your Fair Under Capitalism’s Opportunity score, aka FUCO score. These scores will make all Real and Responsible Americans RICHER THAN EVER BEFORE!! No more excuses!

Your FUCO score will be calculated as shown below:

Old Woke FICO score vs Fair Under Capitalism’s Opportunity score

Your FUCO score will still be somewhere from 300 to 850 to help Major Banks approve your housing, loans, credit, and Life, just like FICO but BETTER! This is a win for all True Patriots!

We cannot confirm how your Patriot record is calculated because National Security says so. But it will happen in real time using the latest corporate, military, and non-rigged voting machine insights. Owning $TRUMP and Trump NFTs will boost your score, while credit card transactions at Gay Bars and halal Food Trucks will hurt you.

There is no affordability crisis because it is a Democrat HOAX! Therefore, a Low FUCO Score will be PROOF that a person is in Antifa (a gang we recently made up) or a childless cat lady. High FUCO means a Bright Secure Future for the USA!! Thank you for your attention to this matter.

— END OF PRESS RELEASE —

Yes, that was fake. Har har har.

But this dystopian satire is based on more facts than you may realize.

Surveillance capitalism is ramping up, between social media monitoring, cameras on every building, and your boss spying on you. But before computers were even a thing, one industry paved the way to you feeling like you’re always being watched (because you are) — consumer credit reporting.

As Josh Lauer explains in his book, Creditworthiness: A History of Consumer Surveillance and Financial Identity in America, “It was not the welfare or protection of the state that spawned the first mass surveillance systems in the United States; it was the security of capitalism.”

The implications for debtors and those who could take on crushing debt at any time (read: all of us) are massive. Here are just a few ways that credit scores and reports can impact all of us in the name of patriotism…

FACT: Credit rating agencies are allowed to falsely label you as a terrorist

Imagine going to take out a car loan just to be denied — not because of a missed payment or too many debts, but because they think you are a terrorist. It’s totally legal, thanks to TransUnion LLC v Ramirez.

In October 2020, the Supreme Court ruled that credit reporting agencies can label you a potential terrorist or drug trafficker without your knowledge, even if you request a copy of your credit report. As noted in the dissent, if you wanted this information included in your copy of your credit report, you’d have to pay TransUnion extra.

The case was brought after TransUnion did this to thousands of borrowers based only on a first and last name. Granted, reporting agencies know your date of birth, middle name, the dream you had last night, and much, much more. They may — as a supposed courtesy — send you a letter that says, “btw, we (the guys who could make it impossible to cover your basic needs at any moment) think you might be on a government watch list for some serious shit. And we won’t say whether you can dispute this. xoxo!”

As if life under American Capitalism’s “Opportunity” doesn’t already require that we be “worthy” of incurring a ton of debt at a moment’s notice — on average, an inpatient stay in the hospital costs $3,297 a night, according to 2024 data from KFF. That gets charged on personal loans, credit cards, hospital repayment plans. Even if you emerge on the other side debt-free, you may feel forced to pay higher health insurance premiums for the rest of your life to keep your out-of-pocket max low. Maybe you’ll skip healthcare altogether.

FACT: The credit reporting industry knows that debt is a way to control you

As noted by Josh Lauer in Creditworthiness, “[Credit] bureau operators viewed themselves as something more than purveyors of a mundane business service; they were patriotic agents of social order” [emphasis added].

One of the key myths that upholds this social order which credit rating agencies rely on is the idea that borrowing is an equal exchange between two parties. Thus, a massive corporation has a right to rate you.

Think about how ridiculous that sounds. A large institution and an individual working-class borrower on the same playing field? Let’s be real — when someone borrows from a major bank or even the federal government (the Department of Education effectively operates as one of the largest predatory lenders in the country), the power dynamics are deeply inequitable.

Despite this disparity, the entire system of creditworthiness is built on the assumption of a fair and equal partnership. Credit scores are then treated as objective measures of responsibility rather than reflections of a system that disproportionately benefits lenders over debtors.

Understanding this imbalance is crucial in order to push back against the U.S. multi-billion dollar credit reporting apparatus. A credit rating absolutely shapes aspects of one’s daily life, but it is not a measure of their value or character. Letting go of shame tied to a low credit score — much like student debt taken on in pursuit of education — is an important step toward reclaiming your power. Through a debtors’ union, we can build collective power towards abolishing our debts and the concept of creditworthiness itself.

So how do we push back against credit reports?

While a low credit score is no laughing matter, it’s worth calling out the hypocrisies of a system that doesn’t need to exist at all. The logic behind credit scoring is so arbitrary that you could easily imagine something like a “true patriot credit score” being introduced and carrying just as much weight as the current system. After all, people are sometimes penalized with a lower credit score after paying off their student debt — hardly a rational measure of so-called financial responsibility.

Stepping back, the bigger picture becomes clear: this system is about control. Credit scores function as a way to surveil, discipline and restrict working-class people’s access to basic needs like housing, healthcare and education.

At the same time, there are examples of successful resistance. Organizers in the healthcare space successfully petitioned to remove medical debt from credit reports, challenging the idea that a medical emergency should follow someone financially for years. Even the backlash to this win reveals how much power is at stake — systems don’t push back unless their power is meaningfully threatened.

As bell hooks reminds us, people will try to destroy you precisely because of your potential power. So as we navigate the financial hellscape, it’s important not only to stay grounded in that awareness, but also to find moments to challenge the system with a bit of humor along the way.

Myriam Robinson-Puche (she/her) is a personal finance freelance writer and a member of Debt Collective's Media, Art and Design team. Myriam has written for Morning Brew, MarketWatch, Bankrate and more. She also previously worked as a financial coach.

| A guest post by

|